Understanding a Balance Sheet - CFO Corner 7/2023

What is a balance sheet?

The balance sheet is one of the three main financial statements, along with the income statement and cash flow statement.

While income statements and cash flow statements show your business’s activity over a period of time, a balance sheet gives a snapshot of your financials at a particular moment in time. It incorporates every journal entry and transaction since your company launched. Your balance sheet shows what your business owns (assets), what it owes (liabilities), and what money is left over for the owners (owner’s equity).

Because it summarizes a business’s finances, the balance sheet is also sometimes called the statement of financial position. Companies usually prepare one at the end of a reporting period, such as a month, quarter, or year.

The purpose of a balance sheet

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. Investors, business owners, and accountants can use this information to give a book value to the business, but it can be used for so much more.

At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

The information in your company’s balance sheet can help you calculate key financial ratios, such as the debt-to-equity ratio, a metric which shows the ability of a business to pay for its debts with equity (the smaller the ratio, the better). Even more immediately applicable is the current ratio: current assets / current liabilities. This will tell you whether you have the ability to pay all your debts in the next 12 months (Rule of thumb; this ratio should be 1x or greater).

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one.

What goes on a balance sheet

At a high level, a balance sheet works the same way across all business types. They are organized into three categories: assets, liabilities, and owner’s equity.

Assets

Let’s start with assets—the things your business owns that have a dollar value.

List your assets in order of liquidity, or how easily they can be turned into cash, sold or consumed. Bank accounts and other cash accounts should come first followed by fixed assets or tangible assets like buildings or equipment with a useful life longer than a year. Even intangible assets like intellectual properties, trademarks, and copyrights should be included. Anything you expect to convert into cash within a year are called current assets.

Current assets include:

Money in a checking account

Money in transit (money being transferred from another account)

Accounts receivable (money owed to you by customers)

Short-term investments

Inventory

Prepaid expenses

Cash equivalents (currency, stocks, and bonds)

Long-term assets (or non-current assets), on the other hand, are things you don’t plan to convert to cash within a year.

Long-term assets include:

Buildings and land

Machinery and equipment (less accumulated depreciation)

Intangible assets like patents, trademarks, copyrights, and goodwill (you would list the market value of what fair price a buyer might purchase these for)

Long-term investments

Let’s say you own an ice cream business called “Sub Zero Ice Cream” (We stretched for a name). As of December 31, your company assets are: money in a checking account, an unpaid invoice for a wedding you just catered, and cookware, dishes and utensils worth $900. Here’s how you’d list your assets on your balance sheet:

Liabilities

Next come your liabilities—your business’s financial obligations and debts.

List your liabilities by their due date. Just like assets, you’ll classify them as current liabilities (due within a year) and non-current liabilities (the due date is more than a year away). These are also known as short-term liabilities and long-term liabilities.

Your current liabilities might include:

Accounts payable (what you owe suppliers for items you bought on credit)

Wages you owe to employees for hours they’ve already worked

Loans that you have to pay back within a year

Taxes owed

Credit card debt

And here are some non-current liabilities:

Loans that you don’t have to pay back within a year

Bonds your company has issued

Returning to our ice cream business example, let’s say you haven’t yet paid the latest invoice from your food supplier. You also have a business loan, which isn’t due for another 18 months.

Here are Sub Zero Ice Cream’s liabilities:

Equity

Equity is money currently held by your company. This category is usually called “owner’s equity” for sole proprietorships and “stockholders’ equity” or “shareholders’ equity” for corporations. It shows what belongs to the business owners and the book value of their investments (like common stock, preferred stock, or bonds).

Owners’ equity includes:

Capital (the amount of money invested into the business by the owners)

Private or public stock

Retained earnings (all your revenue minus all your expenses and distributions since launch)

Equity can also drop when an owner draws money out of the company to pay themself, or when a corporation issues dividends to shareholders.

For Sub Zero Ice Cream, let’s say you invested $2,500 to launch the business last year, and another $2,500 this year. You’ve also taken $9,000 out of the business to pay yourself and you’ve left some profit in the bank.

Here’s a summary of Where’s the Beef’s equity:

*[Retained Earnings is a cumulative figure from P&Ls over time. All Balance Sheet figures are cumulative. In this illustration R/E is determined by taking Total Assets less Total Liabilities adding back Drawing (R/E before the Draw) and deducting Capital (Capital is separate from R/E). So; $9050 - $2150 + $9000 - $5000 = $10,900]

The balance sheet equation

This accounting equation is the key to the balance sheet:

Assets = Liabilities + Owner’s Equity

Assets go on one side, liabilities plus equity go on the other. The two sides must balance—hence the name “balance sheet.”

It makes sense: you pay for your company’s assets by either borrowing money (i.e., increasing your liabilities) or getting money from the owners (equity).

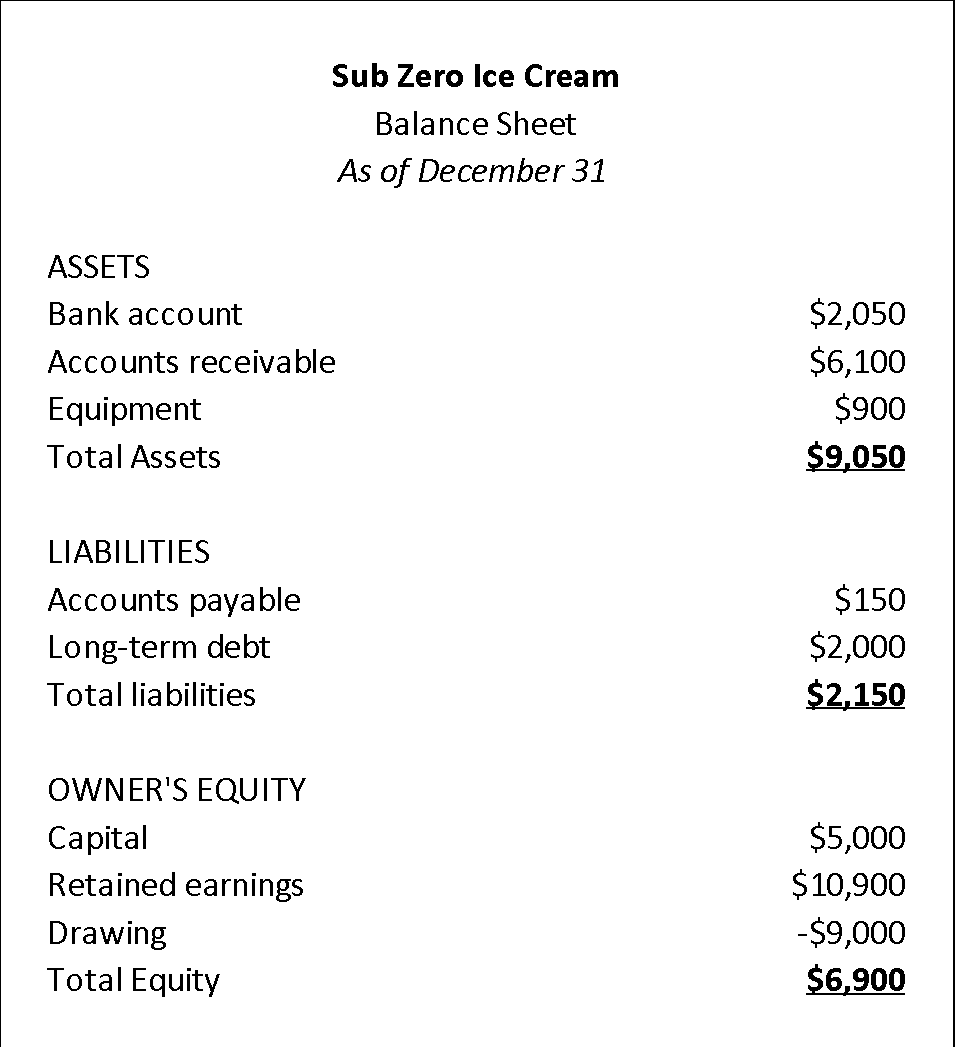

A sample balance sheet

We’re ready to put everything into a standard template. Here’s what a sample balance sheet looks like, in a proper balance sheet format:

Nice. Your balance sheet is ready for action.

Great. Now what do I do with it?

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one.

Here’s some metrics you can calculate using your balance sheet:

Debt-to-equity ratio (D/E ratio): Investors and shareholders are interested in the D/E ratio of a company to understand whether they raise money through investment or debt. A high D/E ratio shows a business relies heavily on loans and financing to raise money. In our scenario, the D/E ratio is 0.31. One could argue that this ratio is ok.

Working capital: This metric shows how much cash you would hold if you paid off all your current, or short-term, debts. It signals to investors and lenders how capable you are to pay down your current liabilities. General, working capital is defined as Current Assets - Current Liabilities. In our scenario, it looks pretty good.

Return on Assets: A formula for calculating how much net income is being earned relative to the assets owned. The more income earned relative to the amount of assets, the higher performing a business is considered to be. In our scenario you would take Net Income from the P&L and divide it into Total Assets. Something on the order of 5%-8% would be good.

By Frances McInnis on February 22, 2022, with edits and additional comments by Rob West, MBA

Related Articles

9 Tips for Managing Small Business Finances - CFO Corner 12/2021

9 Tips for managing small business finances Aggregated by Rob West, CFO, MBA Here are a few things you should do as a small business owner to stay on top of your finances. 1. Pay yourself. If you're running a small business, it can be easy to try and ...10 Small-Business Financial Tips for 2021 - CFO Corner 11/2021

Two businesses. Two smart leadership teams, two motivated staffs, two potential blockbuster products. So why is one growing and the other floundering? Three words: Smart financial planning. Whether you’re a first-time entrepreneur or a business owner ...Payment Preparedness Matrix Model - CFO Corner 8/2021

PAYMENT PREPAREDNESS MATRIX Model (“PPM”) The model is attached below or found linked here. I picked this tip up from Investment Bankers I know. I follow this PPM model and, quite frankly, it has served me very well! I pass this on to you as we are ...10 Financial Tips All Businesses Should Follow - CFO Corner 9/2021

10 Financial Tips All Businesses Should Follow by Rob West, CFO, MBA Sept 1, 2021 Good and effective management of finances makes the difference between a business that succeeds and one that fails at the very first hurdle. Here are some proven ...Financial Reporting Requirements

Statement Requiring Financial Reporting Sub-Zero Franchising requires Financial statements and the following defines what is required. The Franchisor is required by the FTC to audit and publish our books annually. However, your books are confidential ...